From AI Capability to Healthcare Product Strategy

CONTEXT

TO TRANSLATE AN IMAGE-BASED AI SCREENING CAPABILITY INTO A CLEARER HEALTHCARE PRODUCT STRATEGY ACROSS CONSUMER HEALTH, CLINICAL WORKFLOWS, REGULATORY EXPECTATIONS, AND HEALTHCARE ECOSYSTEMS.

PROJECT OVERVIEW

An early-stage company had built an AI-powered health-screening capability with potential reach across consumer wellness, testing, and clinical diagnostics. The technology was promising, but the product direction was wide open, and that turned out not to be a design problem.

The real question was strategic: how does an AI capability become a clear, viable, adoptable product in a market as crowded, regulated, and trust-sensitive as healthcare? Answering it meant looking past the interface to the market, audience expectations, regulatory boundaries, clinical adoption barriers, and ecosystem opportunities around healthcare AI.

I ran a multi-round research program across consumer apps, clinician tools, and the regulatory landscape, and synthesized it into decision-ready frameworks the team could use to choose a direction. This case study covers how I designed that research, the analytical models I built to make a noisy market legible, and the strategic implications that came out of it.

STRATEGIC PROBLEM

The same technology could be interpreted through several product lenses: a consumer wellness tool, a self-directed screening experience, diagnostic support, an HCP workflow tool, a broader AI-imaging platform, or a node within a connected care ecosystem. Each path implied a different audience, experience model, business case, brand narrative, regulatory exposure, and strategy path.

As a result, the brief was not simply to “build trust” around the product. It was to clarify where this capability could create the most value in the healthcare journey, and what product model would make that value credible, usable, and adoptable. The research was organized around six strategic questions:

- Where the product should play?

- Who the primary audience could be?

- What claims would be appropriate?

- Which adoption barriers mattered most?

- What experience patterns were required?

- How broad the opportunity could become?

MY ROLE

I worked with the strategy team to lead competitive, regulatory, and thematic research across multiple rounds of the engagement. My responsibilities included structuring the research approach, conducting analysis and competitor deep dives, mapping the regulatory landscape, and developing synthesis frameworks that translated scattered findings into actionable strategic direction.The work evolved across several rounds, with each phase helping the team and client investigate the areas that required deeper clarity.My contribution was not simply collecting information. It was connecting fragmented signals across business, UX, technology, healthcare, and regulation into a coherent strategic narrative the team could use to evaluate product direction.

APPROACH

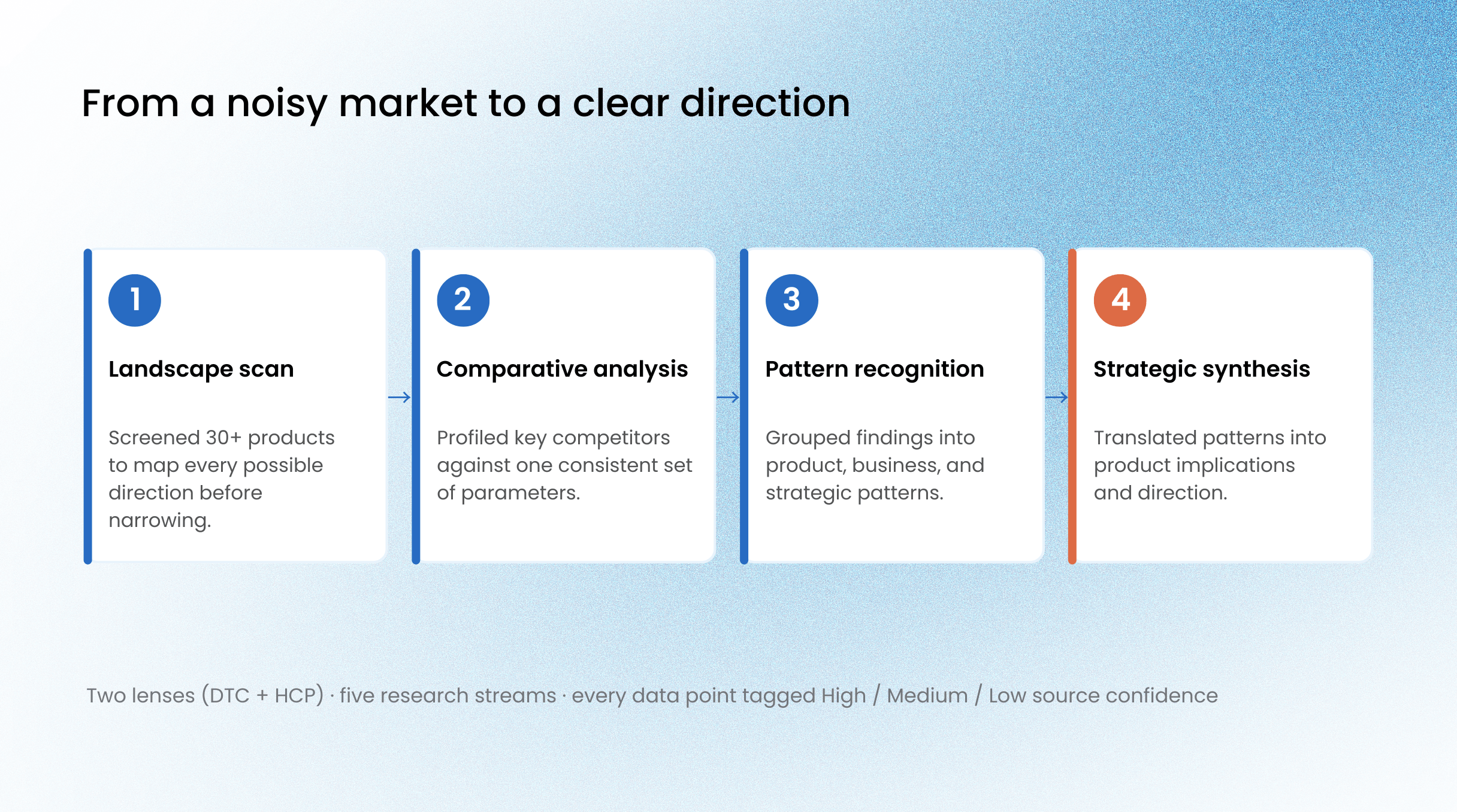

Because the source material varied significantly in quality and reliability, from investor filings and regulatory guidance to marketing pages, app-store reviews, and informal commentary, I began by creating a research structure that made the analysis rigorous, comparable, and trustworthy.

Two lenses, five streams. I organized the landscape through two primary lenses: DTC products and HCP tools. Across both lenses, I studied five connected streams: consumer health products, healthcare-professional tools, regulatory and claims positioning, UX and product-experience patterns, and the broader healthcare ecosystem. Each competitor was evaluated against a consistent set of parameters, including audience, category, functionality, clinical vs. wellness positioning, regulatory signals, technology and AI language, trust cues, UX patterns, business model, market presence, sentiment, workflow integration, and ecosystem fit.

A source-confidence system. Because healthcare information online can range from peer-reviewed studies to informal forum discussions, I tagged each data point as High, Medium, or Low confidence. Peer-reviewed research, government sources, regulatory information, and investor materials were treated as highest confidence; company marketing and product pages as medium confidence; and blogs, forums, and informal commentary as lower confidence. This helped the team weigh evidence appropriately rather than treating all claims as equal.

The work moved through four stages:

Turning research into positioning frameworks. Rather than presenting the work as a set of competitor profiles, I developed analytical models that made the landscape easier to understand at a glance. This became one of the most important parts of the work:

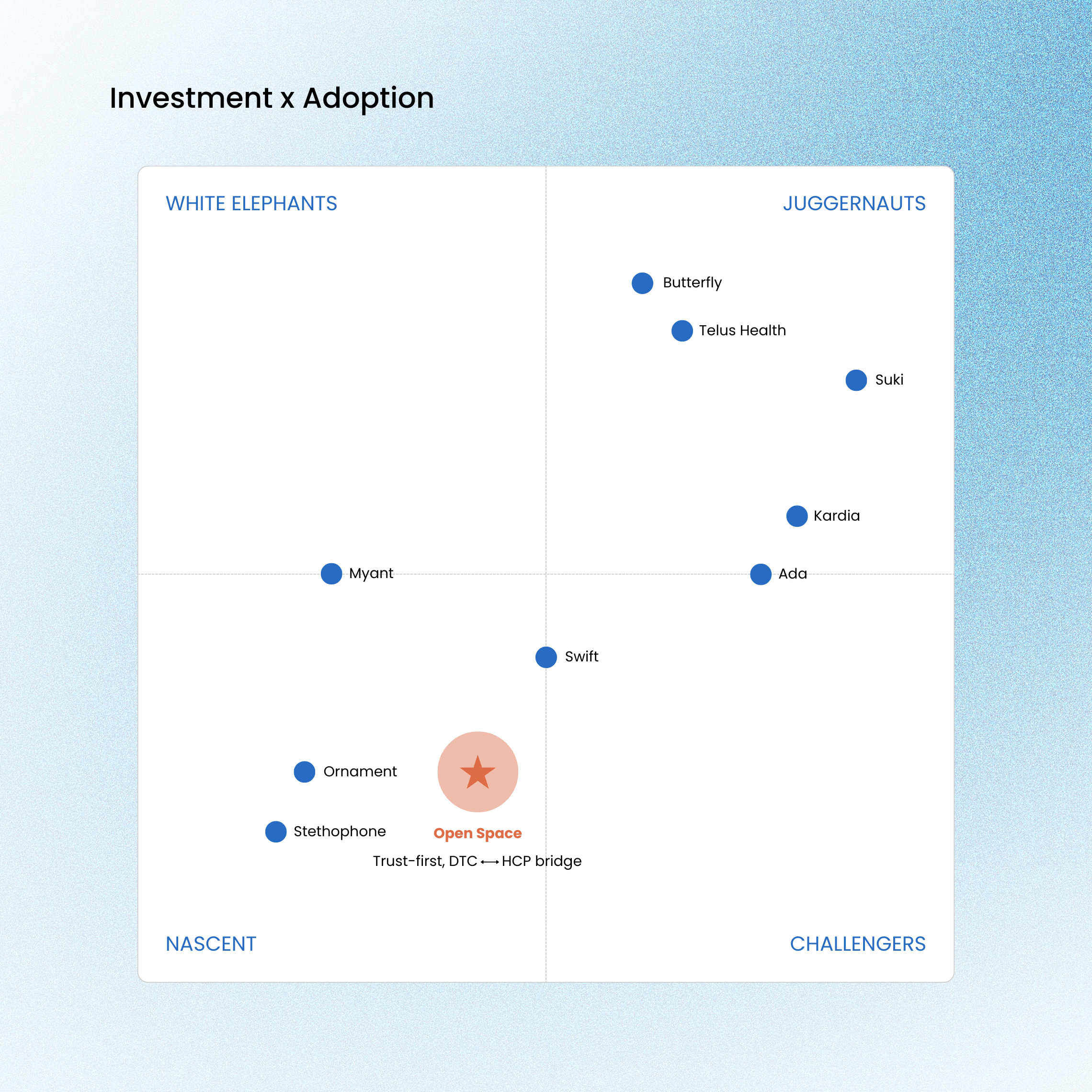

An Investment × Adoption quadrant that grouped players into Juggernauts, Nascent, Challengers, and “White Elephants”, products with strong investment signals but weaker adoption.

The framework helped the client see not only which players existed, but where the market was converging, where it was becoming crowded, and where there may be open strategic territory.

The regulatory question. A core thread of the research was understanding when a product begins to cross into regulated medical-device territory. I reviewed the FDA’s Software as a Medical Device framework, HIPAA, the EU Medical Device Regulation, and standards such as ISO 13485, then mapped the intended product direction against relevant classification criteria. One strategically important finding was that many consumer apps position themselves as “non-diagnostic” while still holding medical-device certifications. This reinforced that regulatory exposure is not determined by positioning language alone; intended use, functionality, claims, and user guidance all shape how a product may be understood or regulated.

The final interface brings together destination discovery, curated recommendations, booking details, payment, confirmation, and trip management in one mobile experience. The design uses a warm visual system, illustration, and image-led layouts to create a travel experience that feels guided, approachable, and culturally inspired.

RESEARCH FINDINGS

Across the landscape, a consistent set of patterns separated products that appeared credible and adoptable from those that felt unclear, fragmented, or difficult to trust.

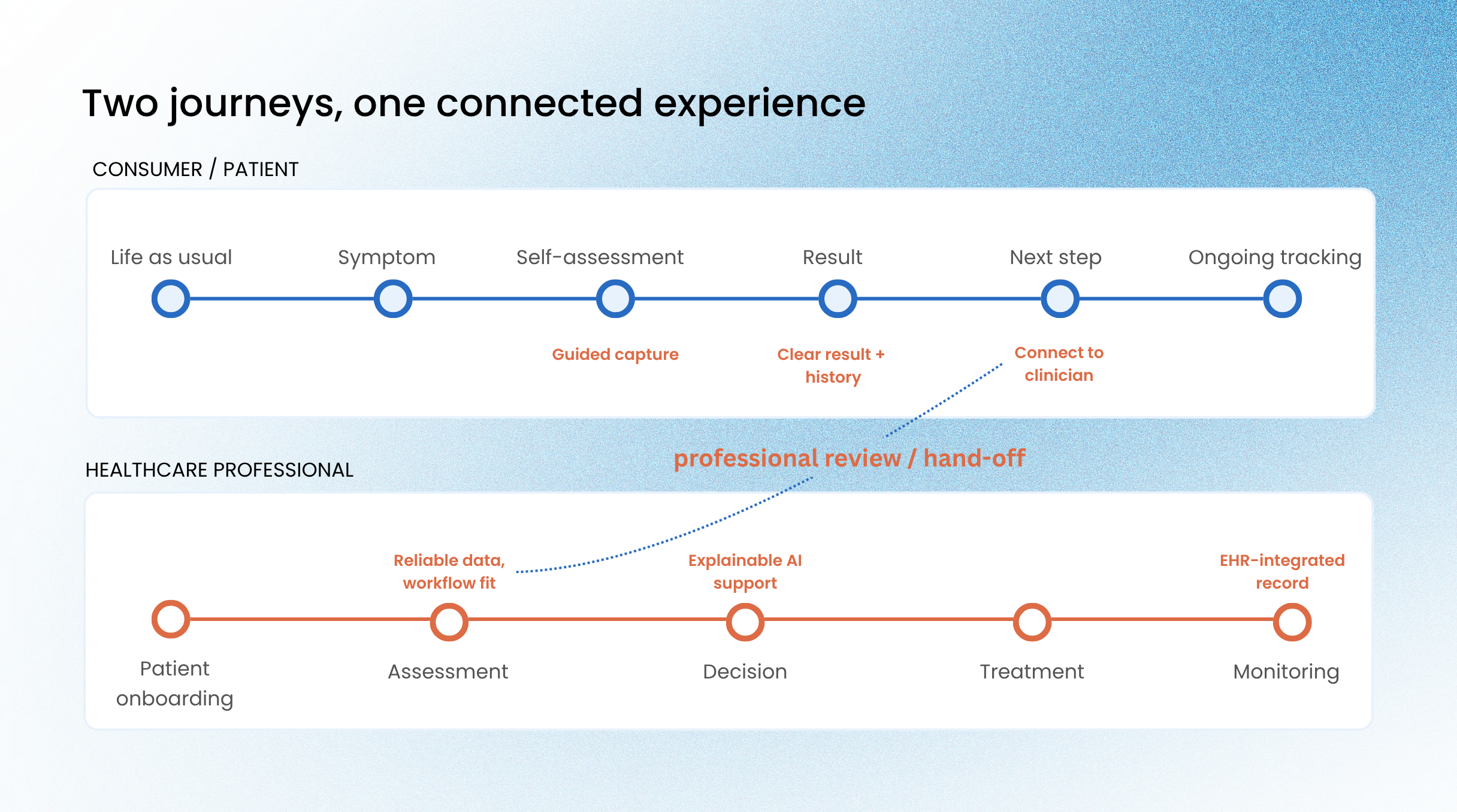

On the consumer side, trust emerged as a gating factor. Users need more than features; they need scientific backing, transparent data practices, clear limitations, and understandable AI. Focused products performed better than feature-heavy experiences that overwhelmed users with too much data or unclear functionality. Because many of these tools depend on user-submitted input, guided capture became a core product capability, not a secondary UX detail. I

If users cannot capture a clear, well-framed image, the experience becomes unreliable before the AI analysis even begins. History dashboards and shareable reports also created longer-term value by turning one-time results into trackable health records and reasons to return. Patient autonomy represented a meaningful opportunity, but the closer a product moved toward medical interpretation, the more users needed reassurance, clear boundaries, and a path to professional follow-up.

On the clinician side, adoption depended on workflow fit. HCPs do not adopt AI because it is new; they adopt it when it reduces burden, supports decision-making, and fits into existing clinical realities. The strongest tools integrated into workflows clinicians already understood, such as bidirectional EHR sync, familiar interface patterns, and AI that reduced uncertainty rather than adding complexity. Skepticism was often tied to liability, regulatory ambiguity, bias, and the black-box nature of AI. As a result, explainability and augmentation became essential. In clinical contexts, AI needed to support professional judgment, not replace it. Tools that influenced diagnosis carried a higher bar for evidence, validation, integration, and accountability.

Across both audiences, claims strategy became a product-risk issue. If a product behaves like a medical device, users, clinicians, and regulators may evaluate it that way regardless of softer marketing language. The research also suggested that the strongest opportunity was not a standalone app, but a connected model linking consumer capture, AI-supported screening, health history, professional review, and care pathways.

STRATEGIC TENSION

Several tensions shaped the direction, each with a clear implication.

DTC reach vs. clinical credibility. Consumer reach drives accessibility and earlier action; clinical credibility drives trust but demands evidence, integration, and validation. Implication: the product can't rely on one audience strategy; it has to speak to both, differently.

Wellness positioning vs. diagnostic value. Wellness language feels accessible but can undersell a screening product; diagnostic language signals value but raises the bar on evidence, regulation, and liability. Implication: claims must precisely match actual functionality.

AI innovation vs. healthcare usefulness. An AI-first story sounds advanced, but in healthcare the technology only matters for the outcome it supports. Implication: shift the story from "advanced AI" to "practical healthcare value."

Standalone app vs. connected ecosystem. A standalone app is easier to launch, but value often lives in what happens after the result. Implication: the strongest opportunity bridges consumer action and professional care.

Speed vs. responsibility. Fast results only create value when users understand them and know what to do next. Implication: balance convenience with careful communication and follow-through.

SYNTHESIS AND DIRECTION

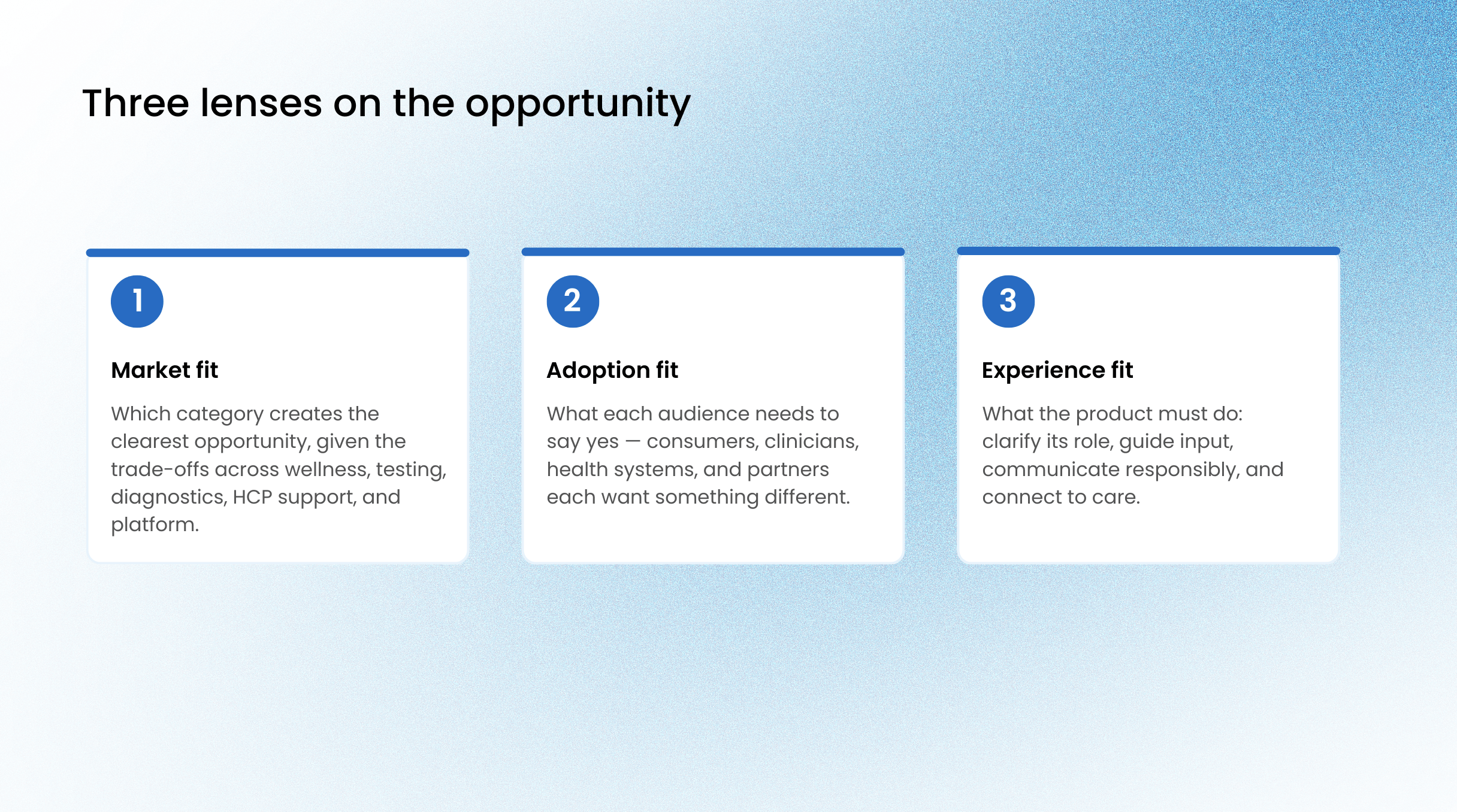

Across the research, I pulled the findings together through three lenses, each answering a different question about where this capability could win.

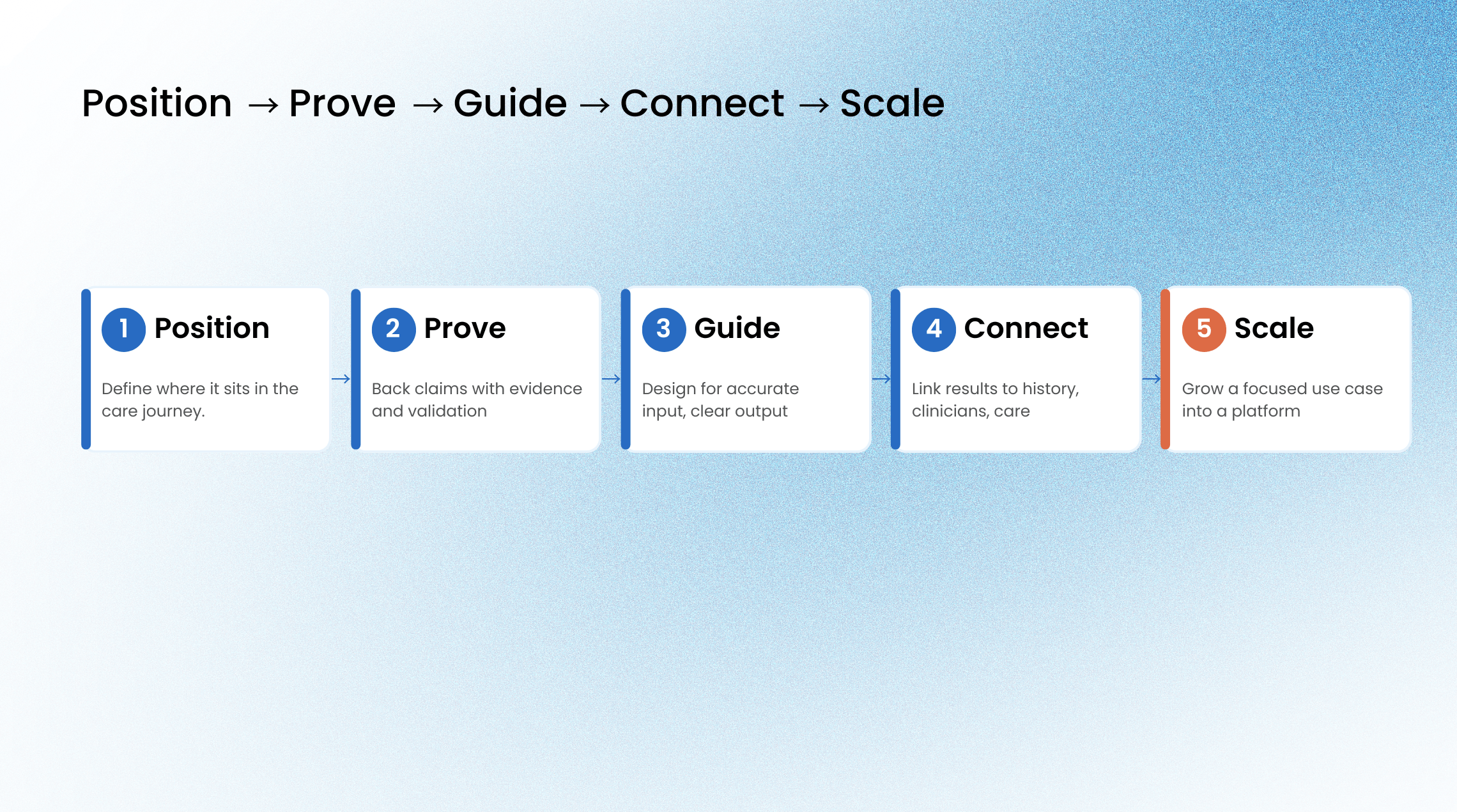

Read together, the three lenses pointed toward a direction that balances consumer accessibility with clinical credibility: a product accessible enough for self-directed users, credible enough for professional adoption, and defined by the healthcare problem it solves rather than by the AI underneath it.To make that direction something the team could build against, I framed it as a simple spine: position the product clearly in the care journey, prove its claims with evidence and appropriate validation, guide users toward accurate input and understandable output, connect results to history, clinicians, and care pathways, and scale from a focused use case toward a broader platform.

OUTCOME

The research did not end as a report. It gave the client a shared map of a noisy market, a common vocabulary for weighing trade-offs, and a defensible direction to commit to, shifting the conversation from "can we show the AI works" to "where this product creates the most value, and how to make it credible and adoptable."That direction fed into the product strategy the client chose to pursue. They have since moved from exploration into building the product, carrying the positioning, audience, and experience priorities from this research into development.

REFLECTION

This project shifted how I understand UX and CX research .The work was not about screens first. It was about making sense of a complex product opportunity where market signals, business goals, healthcare realities, regulatory constraints, and user experience all had to be considered together.In healthcare AI, usability is only one part of the question. A product also has to be understandable, credible, adoptable, and connected to a real care pathway. Without that, even a strong AI capability can remain just a technology.My biggest takeaway was that product value does not come from the AI itself. It comes from knowing where the technology belongs, who it serves, what decisions it supports, and how responsibly it fits into the healthcare journey.